Applying the tax-efficient waterfall requires elbow grease and knowing just enough jargon to get what you need. Let’s break down our waterfall and how to piece together what you need:

Tax-efficient savings at work. For most physicians, the bulk of your savings will be in retirement plans at work. In fact, many hospitals are beefing up plans to allow over $100,000 in tax-efficient savings! In those cases, probably ALL retirement savings will be happening at work.

Let’s start there. Here is the email I would send. I find humor is always helpful. You might be overwhelmed by the jargon, but don’t be surprised if you find HR professionals are just as overwhelmed, if not a little rusty. Not nearly enough physicians take advantage of all the retirement plans, so you might be the first person to ask questions about them in a while.

“Good morning,

Over the weekend, I endured an entire presentation on tax-deferred savings strategies, and I want to make sure I don’t miss out on any opportunities here to take full advantage.

First of all, can you please confirm that I am maxing out my 403(b) or 401(k)? When the federal maximum savings increases, do I need to contact you at the beginning of the year to confirm that my contributions are going up to take full advantage?

Are there additional plans available, like a 457(b) or a non-qualified deferred comp plan? Can you confirm if I am maxing out those as well? If not, can you please point me to the right person to help me set that up?

Am I in a healthcare plan that has the option for an HSA? If so, I would like to save into that and invest those funds. Am I on track to do that?

Are there any other retirement savings vehicles like mega backdoor Roths available? If so, can you point me to the right person to help me set that up?

Thank you!”

If you work for yourself or as a 1099 contractor, I want you to consider setting up your own Solo 401(k). It’s never been easier to start your own plan. I promise! Here is a tutorial.

Credit card debt: Pay it off. Aggressively.

Student loan debt: Pay it off. Aggressively. Or make sure you are pursuing Public Service Loan Forgiveness (PSLF) and dotting every I and crossing every T. Lower your payments through filing separately if that makes sense. Choose your repayment plan that is eligible for PSLF and offers the lowest payment. Certify employment annually. Keep this on the front burner until those loans are gone.

Backdoor Roth. Fun little maneuver, but only for the real tax-efficient nerds. Here is a great tutorial. Also, here is permission to skip and move to the next one if you look at that tutorial and think, “No way.”

Taxable brokerage account. This is where you open up some account at a place like Vanguard, Schwab, or Fidelity, and you invest in a regular old account with no tax whistles. We call these brokerage accounts.

The big question here is “To DIY or Not To DIY.” The TLDR here is that you need to discern what you want in a relationship with your money. For most physicians, we find the optimal decision is to have a close relationship with their account and manage it themselves. For some, that sounds initially scary, but trust me, it’s never been a better time to do it yourself. But just because you want to be involved doesn’t mean you have to go out and do it alone.

Advice-only firms are designed to hand-hold you in executing on this step. Advice-only financial planners give clear instructions on what to do and support you along the way.

The Not To DIY is delegating to a Fee-only firm that will want to take the money and invest it. You become a bit less connected to the money and the plan, typically pay much higher fees, and risk a conflicted advisory relationship. For example, the advisor likely only makes money charging a percentage fee on the brokerage account, so they might find themselves disinclined to support the decision you make to maximize your tax-efficient options that they can’t derive a fee on.

The main takeaway here is to focus on the plans at work right now. Don’t get bogged down by the buckets at the bottom of the waterfall. Once you get the work plans set up and automated and your student loans on track for payoff or PSLF, you will probably feel some momentum to tackle the other buckets, anyway.

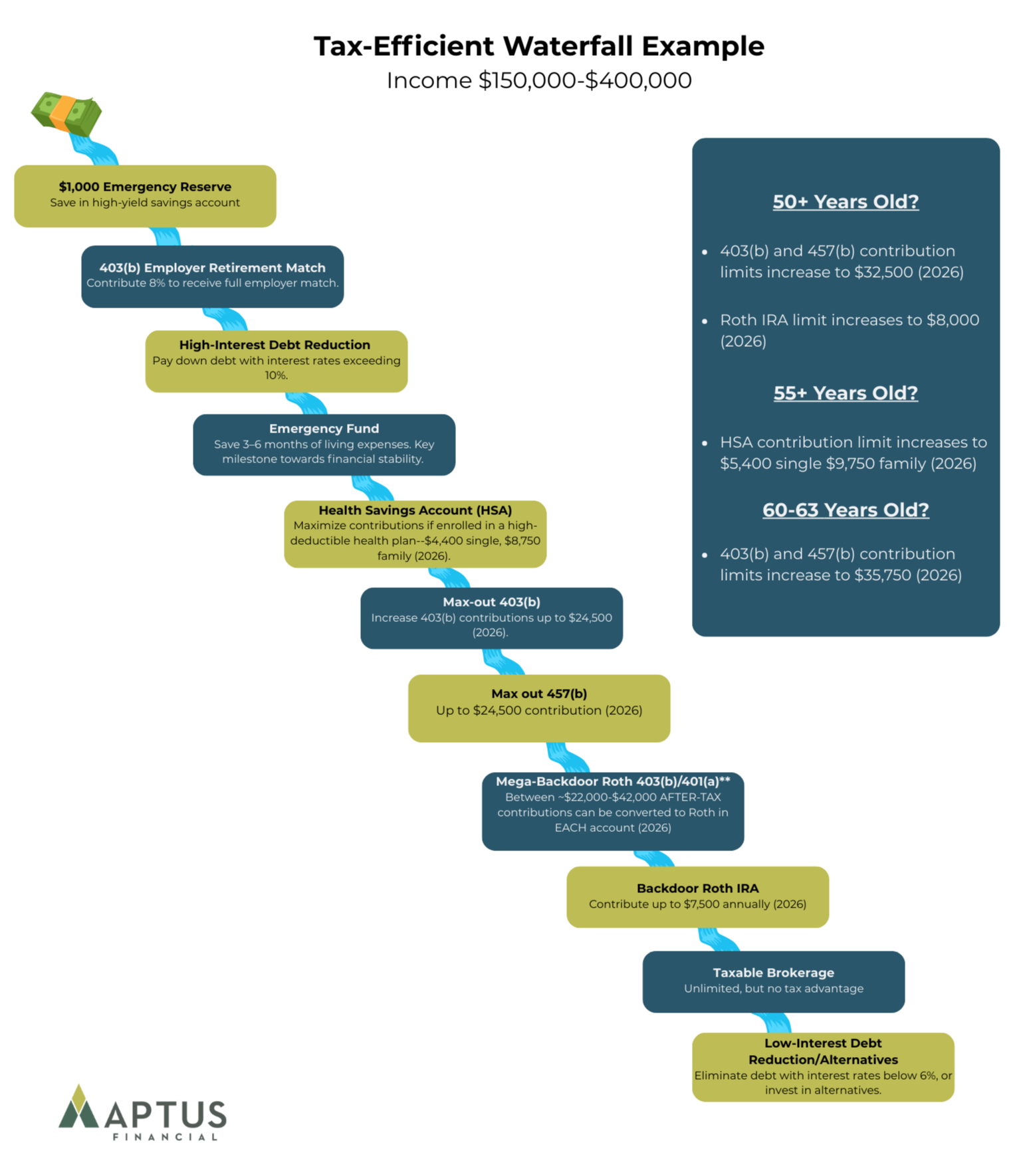

Want to see the Tax-Efficient Waterfall at work?

Let’s take someone working for an institution that has a 403(b) with a match of 50% up to 8%, a 457(b), an investable HSA, and the option for mega backdoor Roths. Note that the first box is emergency reserves of $1,000. We want people to have a small starter pile of cash available before starting an aggressive tax-efficient strategy. After that initial nest egg is built, we assume physicians continue to add to liquid savings for near-term emergencies.

Keep it simple, folks. Just follow each bucket one by one. Ask the right people the right questions and apply your savings to the most tax-advantaged buckets available to you.

And remember, the right answer is not to shove this to the back burner. The best alternative to a back burner is seeking the help of a financial planner. This could save you time and mistakes, but more importantly, make sure that these important investments get made and not delayed. If you are intrigued by the idea but not sure if it’s right, you can set up a complementary diagnostic call with an Aptus planner. They can see where you are, and if you are the right candidate for Advice-only financial planning, they will walk you through what would be accomplished in that relationship.