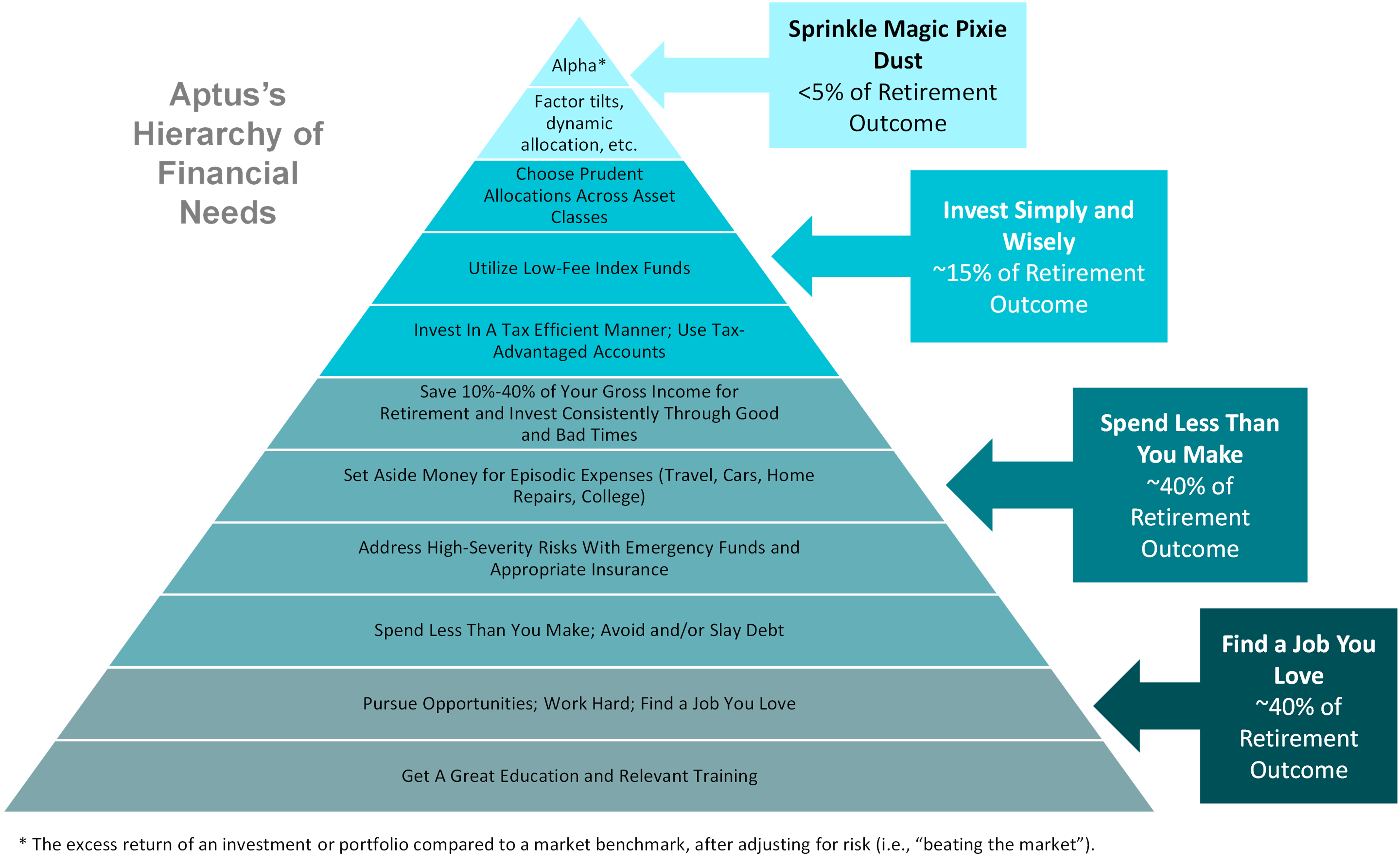

A lot of people who call themselves financial advisors will try to talk your ear off about investing. Boooooring. Hey, I love investing as much as any red-blooded finance nerd but that's not the key to building a strong financial foundation. In Aptus’s Hierarchy of Financial Needs, a concept we first wrote about in 2017, we think your energy is better spent on finding a job you love, spending less than you make and investing simply and wisely. Magic pixie dust is very optional.

Find a job you love.

We spend a lot of our waking hours pursuing our careers. Life is too short and precious for those hours at work to be miserable. We should always consider the possibility of finding, creating or striving towards a new, more fulfilling career. Some folks are born with the wind at their back while others face challenges I can barely imagine. Regardless, I believe everyone has an opportunity to improve their situation. If you work hard, study diligently and pursue opportunities, you might be able to find a job you love—or at least don’t hate. If you love your job, you’ll likely perform well, stick with it and find some fulfillment. If the job happens to pay well, all the better.

Spend less than you make.

We have clients across all income levels who struggle with overspending and under-saving. It’s rarely a problem fixed by simply making more money. When people are under-saving, pay raises often just fuel higher spending. Most folks in the lowest quartile of household income struggle to make ends meet and can credibly say they could save more if they made more. For the rest of us, though, it’s human behavior rather than circumstance that drives our spending and savings habits. We recommend adopting and implementing a cash flow system to help sharpen your savings calculations. Start by saving 10%-plus of your pay for retirement and probably more like 20%-40% if you’re a high earner and/or getting a bit of a late start. Make sure to utilize tax-advantaged savings accounts like 401(k)s and IRAs. It’s also critical to save into an emergency fund and other savings accounts to address both known and unknown future expenses. If you save appropriately, you can screw up a lot of other things and still retire comfortably.

Invest simply and wisely.

We believe that investing, if done well, is relatively easy. We encourage our clients to capture broad market returns by buying a small number of low-fee index funds. Especially for younger investors, we principally focus on stock index funds and bond index funds. Older and higher net worth investors might consider alternative investments like inflation-protected securities or real estate. Our asset allocation recommendations are primarily informed by the averages of a host of target-date fund families. We are trying to take a balanced, humble approach to investing. We are not trying, in any way, to outsmart the market. Perhaps most importantly, though, we believe you should "set it and forget it." Continue to invest in good and bad times. Don’t be swayed by fear or greed.

Sprinkle magic pixie dust?

It’s hard to find a job I love, spend less than I make and patiently invest simply and wisely. That takes too much time. Isn’t there a magic, super-complex investing strategy that will make me richer faster? Sorry, but no. It’s a truism of investing that you don’t get returns without taking risk. If you want higher returns, you have to accept greater risk. Is it possible to beat the market on a risk-adjusted basis in a world with massive computing power, widely available broadband, near-instant dissemination of information, and frighteningly advanced artificial intelligence? Maybe, maybe not. It’s missing the point, though, isn’t it? If you focus on the base of the Hierarchy of Financial needs, we think you will get 95%+ of the way to an optimized retirement outcome. Is it really worth adding complexity and fees to chase that potential last 5%? Probably not.