Physicians typically pay a lot in taxes, but they can sometimes miss out on tax-efficient investing simply because it can feel complicated.

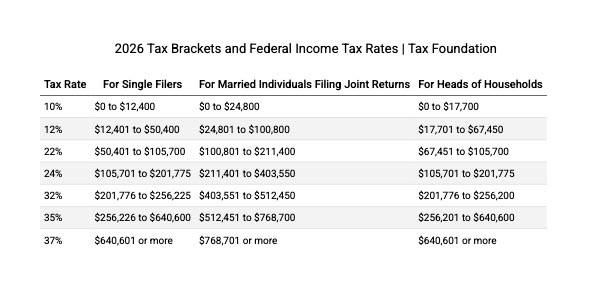

Let us help uncomplicate it. Let’s start with the tax code. The first dollars you earn get taxed gently, but by the time you hit the top brackets, Uncle Sam and your state are basically splitting dessert with you. It’s a progressive system, which is a nice way of saying: “Congrats on your success—now share more of it.”

This is why many physicians look at their W-2 at the end of the year and realize in shock that they paid taxes that would have been an entire salary in training.

Enter why tax efficiency is a game-changer for docs.

Many physicians have two choices: pre-tax and Roth

Pre-tax or Traditional 403(b)/457(b)/401(k) is tax deferred savings. Whatever you put into that account does not get taxed. Instead, you save dollars into the plan and get an immediate tax deduction in your check. The government is signaling toyou to save more than you would otherwise right now with the leverage on your savings dollars. This type of account is king for so many of you right now, because you are saving the most expensive tax dollars. Many of you are bumping into the 32%+ federal tax brackets.

Of course, you then are a co-owner of your account with Uncle Sam. Luckily, you are in the driver’s seat. You are investing that money, growing that money. You pay taxes on the money only when you go to withdraw it, so we see two unique advantages to this strategy. First, you have a larger base of money since you got to grow money you would have otherwise paid in taxes. Second, we presume the withdrawals will be lower than the income you are making, so even if tax rates go up, your marginal rates could be lower.

For many organizations, there is a 403(b) and a non-qualified 457(b). These plans might look similar, but it’s important to understand the differences. There are different withdrawal rules, and a non-qualified 457(b) plan can technically be considered subject to the claims of creditors of the organization. We think it can still be a terrific tool for tax efficiency but want physicians to first feel comfortable with the financial stability of the organization before contributing.

Roth money gets taxed but grows tax-free. Any money you can put into Roth is going to be valuable in retirement because you don’t have Uncle Sam as a co-owner on your account. You don’t have to pay him back later. What you see in this account is what you get.

While we think most physicians should prioritize tax-deferred savings to Roth, many don’t have to make an either/or choice, especially when they work for innovative hospitals and employers adding a megabackdoor Roth.

In this situation, additional contributions can be made beyond the federal limits into the retirement plan via after-tax contributions, and then those contributions can be immediately converted to a Roth IRA.

To learn more about how we prioritize all the options, from paying off student loans to using the tax-advantaged savings, check out our tax-efficient waterfall blog.